China's Quantum Leap Forward

On the Significance of Xi Jinping Thought on China and its Development

Xi Jinping, the current Paramount Leader of the People’s Republic of China, is subject to extensive scrutiny and has been a topic of interest for the Left around the world. His actions have labeled him as the “end of Reform and Opening Up”, while simultaneously being described as the harbinger of a “new dawn of Marxism” in China, or internationally. This article is meant to go into the great significance of Xi Jinping Thought on Socialism with Chinese Characteristics for a New Era, and what it has done materially to help improve the lives of the Chinese people.

This article is the fourth part of RTSG’s series of articles exploring China and her economy, with previous articles covering China’s state-owned enterprises, China’s financial system and economic growth, and China’s corporate governance.

What does a ‘New Era’ actually refer to?

First, we have to establish what is the “New Era” that is being referred to in Xi Jinping Thought. According to Xi Jinping’s own words, it seems to imply that this new era is in which,

“China's reform has entered a deep-water zone, where problems crying to be resolved are all difficult ones” [1]

It is evident that in this New Era, the problems that face China are new and difficult. As a consequence,

“China has reached a new historical starting point. It is a new starting point for China to deepen reform across the board and foster new drivers of economic and social development. It is a new starting point for China to adapt its economy to a new normal and transform its growth model. It is a new starting point for China to further integrate itself into the world and open itself wider to the world.” [2]

I am sure many of the readers know the issues that affected China during Xi’s appointment. Corruption in the lower cadres of the CPC, bureaucratic red tape, environmental issues stemming from industrial pollution, and the influence of the Liberal fifth column within Chinese socio-political discourse, just to name a few.

Xi Jinping is opening a new chapter in New China’s history, hence why it is a ‘New Era’. He is carving forward a path that has broken with the old form of Chinese Marxism, innovating, reforming, adapting and most importantly, improving. Xi Jinping’s Thought is the theoretical realization of “Chinese Socialism 3.0”

This new era was officially declared and cemented into the constitution in March of 2018 after the first Session of the 19th National Party Congress. [3]

Mao Zedong created “Socialism 1.0”, Deng created “Socialism 2.0” and now it is Xi’s turn. There is a saying in China:

Mao Zedong made the Chinese nation stand up, Deng Xiaoping made the Chinese people rich, and Xi Jinping will make the Chinese people strong. [4]

On the Legacy of Mao & Legacy of Deng

Prior to the rise of Xi Jinping, there was a crisis of opinion on the role of Reform and Opening Up. Many of the “Left Deviation” denied the successes and achievements of the post-Deng period. While many of the “Right deviation” denied the success and achievements of the Mao period. What Xi Jinping instituted has been termed the Two Cannot Denies.

“We cannot use the historical period after Reform and Opening Up to deny the historical period before Reform and Opening Up. Neither can we use the historical period before Reform and Opening Up to deny the historical period after Reform and Opening Up”

— General Secretary Xi Jinping [5]

The Communist Party cannot overlook or even conceal the mistakes of Mao Zedong. At the same time, the CPC can also not artificially exaggerate the mistakes of Mao Zedong. If this occurs, the CPC will have violated historical fact and the will of the people; entering into historical nihilism. [6]

The lessons of the perils of historical nihilism are something that is itself a separate discussion. This topic has been briefly touched upon on RTSG’s X (formerly Twitter), within the Russian context. It has also been extensively examined in Chinese scientific political academic circles and Chinese documentaries. The greatest lesson of which could be witnessed in the Soviet Union, in the aftermath of “De-Stalinization”, the leadup to Gorbachev, and the eventual collapse. We recommend examining the hyperlinked content to better understand historical nihilism. To briefly define historical nihilism, it is abstracting one’s national/civilizational history, derooting it from its past and historical lineage by rejecting and outright denouncing it either fully or partially. Such examples include the denouncement of Cromwell by British liberals, the denouncement of the Founding Fathers by American liberals, the denouncement of 1300 years of post-Islamic history by Iranian liberals, or de-Stalinization in the Soviet Union.

According to Professor Feng Wuzhong, Doctor of Marxism at Tsinghua University, there are four broad political positions today in relation to the nature of reform and opening up, represented as Mao Zedong era and the Deng Xiaoping era. [7]

The “Ultra-left” in China upholds the Mao era and Mao Zedong Thought but rejects the Deng Xiaoping era and Socialism with Chinese characteristics (SWCC). This position must be “profoundly re-examined”. The “Left”, which upholds both the Mao and Deng eras, Mao Zedong Thought and SWCC. This position must be “strongly promoted”. [7]

The “Right” in China rejects Mao and Mao Zedong Thought but upholds Deng Xiaoping and SWCC. This position must also be “profoundly re-examined”. And finally, the “Ultra-right”, which rejects both the Mao and Deng eras, Mao Zedong Thought and SWCC. This position must be "firmly opposed". [7]

This indicates that while the “Ultra-Left” and “Right positions” are tolerated or be brought back into the fold of the “Left”, the “Ultra-Right” which seeks to engage in a potential counter-revolution, seeking to “change China’s color”, must be entirely opposed.

The Return of Co-operatives

")

Co-Operative enterprises played a huge role during the Mao Zedong and Deng Xiaoping era, with the formation of agricultural cooperatives being the basis for land reform. And for Deng, the township and village enterprises were the basis for improving rural industrialization, while simultaneously helping poverty alleviation. Though, in the 1990s, the popularity of the co-operatives has since gradually declined.

It was only until around 2007 under Hu Jintao that there were new laws promoting and strengthening rural cooperatives, incentivizing the horizontal integration of the small cooperatives into larger and larger joint cooperative entities [8]. However, their popularity has surged since Xi Jinping’s tenure.

In 2015, the Central Committee of the CPC released a statement based around the improvement and strengthening of the Supply and Marketing Cooperatives. The purpose of this being to accelerate the modernization of agriculture, increase farmers’ income, and promote the construction of a comprehensive moderately prosperous society in rural areas. [9]

The coverage rate of Ningxia’s township supply and marketing cooperatives has increased from 56% in 2017 to the current 92.7%. In 2021, Chongqing's rural comprehensive service cooperatives increased to 6,120, and in administrative villages, the coverage rate reached 76%. [10]

In 2019, the number of household memberships in cooperatives reached 66.828 million, and the size of memberships expanded by nearly 17 times, with an average annual growth of 32.8 percent [11]. Assuming that the average single household contains 2.92 people [12], multiplying that by 66.828 million households, we get 195 million workers, which is 25.84% of the total Chinese workforce (754.47 million) in 2019 [13].

In 2020, Xi Jinping made another statement regarding Supply and Marketing Cooperatives. This further reinforced the point that the cooperatives are a vehicle of agricultural modernization to improve capital efficiency and productivity in agriculture. At the same time, cooperatives are being used for the sake of rural revitalization to close the rural-urban gap/divide. This would make further contributions to the livelihoods of rural citizens. [14]

In 2021, documents were released by 17 different Chinese cooperatives titled the “Implementation Opinions on Carrying out the Construction and Improvement of the Supply and Marketing Cooperative County Circulation Service Network”. According to it, the supply and marketing system should improve the county circulation service network of supply and marketing cooperatives. This is to be done by carrying out actions to improve the three-level county circulation with the backbone circulation enterprises as the support, the county as the hub, the township as the node, and the village level as the terminal. Service networks strive to realize that counties have logistics distribution centers and chain supermarkets, towns have comprehensive supermarkets, and villages have comprehensive service cooperatives. [15]

And subsequently in 2022, the All-China Federation for Supply and Marketing Cooperatives released a statement about deploying more and more civil servants to assist cooperative construction in rural areas, encouraging more of them to take the civil servant examination for the purpose of aiding in rural revitalization. [16]

A few of the positive results of the Co-Ops include helping secure higher income for farmers and increase their purchasing power. Simultaneously, they help provide a rural supply chain, providing more goods in support of the rural regions. [17]

During the outbreak of COVID-19, it might have taken more time for supplies to reach rural regions under lockdown, however Cooperatives helped foot the bill. Co-Ops also respond to government directives to quickly organize production or agricultural supplies during critical shortages. For instance, on August 6th of 2021, Co-Ops were quickly coordinated by the government to rapidly shell out fertilizer produce to ensure the supply of agricultural materials. This was used to quickly recover agricultural production after the event of a natural disaster. [18]

Co-Ops are also used as tools to provide large-scale, professional, and menu-based services to new agricultural business entities and small farmers. They focus on reducing the number of chemical fertilizers and increasing efficiency, preventing pests and diseases, and preventing natural disasters, so as to promote the increase in agricultural production. Co-Ops also helped collaborate with Party Committees to engage in rice monitoring and early warning and cooperated with market supervision departments to crack down on price gouging and price speculation. This means that Co-Ops also serve a dual role as a market disciplinary tool. They help assist the CPC in ensuring prices of agricultural produce does not suffer from bad faith actors price gouging products and preventing the rapid inflating of food prices (in particular rice). [19]

However, while not every farmer has joined a cooperative, it does not mean that their land is somehow being expropriated; the land is still collectively owned by the village of which they reside and farm in. These non-co-op farmers live on their own small family farm for subsistence and occasionally sell their goods for revenue. 98% of all agricultural businesses in China are run by small farmers. Small farmers account for 90% of agricultural employees, and the cultivated land area operated by small farmers accounts for 70% of the total cultivated land area. [20]

All small farmers are either part of a cooperative or work on a family farm, of which the government is trying to encourage and push much more heavily for family farmers to join and form cooperatives. And the CPC encourages and tries to find more ways to support the rural peasantry in the countryside to improve their labor productivity and upgrade their capital efficiency.

In short, we can clearly see that Xi is bringing back a formerly perceived “outmoded” or “obsolete” form of enterprise back into the limelight. The CPC under Xi uses Cooperatives for the purpose of economic revitalization of the rural regions, and as a way to improve the productive forces in the realm of agriculture. The Cooperative enterprises continue to make their contribution to the development of the People’s Republic.

On the Housing/Real Estate Question

The infamous statement said at the 19th party congress in 2017, “Houses are for living in, not for speculation”, has caused profound changes and has shaken the foundation of the Chinese economy. This speculation in housing was exacerbated by local governments’ over-reliance on “land finance”, the phenomenon of selling land to property developers in auctions. This caused property developers to increase the price of apartments to cover the costs, while simultaneously taking out large loans from State banks, meaning the vast majority of their assets became liabilities. And the fact that there is almost no tax burden on real estate holdings meant certain individuals would buy multiple houses as a form of property investment to resell the houses for higher profits. [21]

And so, what are the direct consequences of Xi Jinping’s statement? The Chinese government issued the regulation known as the “Three Red Lines”, which provides three key indicators of the financial health of real estate developers. The Three Red Lines being a liability-to-asset ratio (excluding presales) of no more than 70%; a net debt-to-equity ratio of under 100%; and cash holdings at least equal to short-term debt. This was done to prevent corporations from taking out large loans with no intention of paying the bank back. [22]

The turning point happened in 2021, with the demolition of Evergrande. Evergrande’s billionaire chairman Xu Jiayin was in the Party, and since China is “corrupt” or “capitalist”, surely they’d bail out Evergrande. Right?

No, Xu found that his membership card didn’t help him one bit. The government started dismantling the real estate giant instead. The Wall Street Journal called it a “controlled implosion”. Evergrande was compelled to sell off assets to other companies. However, this presented a problem. What about the houses Evergrande had not yet finished but were meant to be sold to homebuyers? [23]

When Evergrande went bust, their new homes weren’t finished. This understandably made a lot of people angry. So, they went on a mortgage strike. Tens of thousands of homebuyers across dozens of cities in China collectively stopped paying their debt in the summer of 2022, demanding that their homes be completed first. [24]

And since China is “so authoritarian”, surely China would crack down on these “mortgage strikes”, right? Wrong. A few months later, the strike hadn’t been crushed or curtailed. It expanded instead. [25]

But what did China do as a response? Regulators vowed to meet the strikers’ demands, and the government instituted forbearance, meaning that missed payments wouldn’t negatively impact credit scores. [26]

China also instituted 5% annual price ceilings for increase in rent to improve household affordability [27]. Besides controlling financial speculation, the Chinese government has promoted a series of policies for the development of social housing.

The Xiamen government, in Fujian province, reduced the market price by 45% of 4,000 apartments. The Henan government bought 1,050 flats from Evergrande, whose construction was interrupted due to its liquidity issues. In general terms, the Chinese government is supplying 6.5 million new low-cost rental housing across 40 major cities, which started in 2021-2025, to ease housing difficulties for 13 million young people; tier-one cities like Beijing and Shanghai will supply a total of 1.87 million units of low-cost rental housing. In 2021 alone, 936,000 units provided housing for 2 million young people in 40 cities. [28]

In 2023, Beijing has in recent weeks named two “big projects” as the center of its housing policy: building social housing and renovating run-down inner-city districts. The projects have top-level political backing and could soon have 1 trillion yuan ($138 billion) or more of central government support behind them. Renovating urban villages in 35 cities could mean 150 million square meters of new housing per year, which would help drive 10% growth in the area of newly-started property in 2024, reversing a 23% plunge in 2023. [29]

The Western press would like you to believe that the CPC’s new regulations on business and economic intervention by the government are driven by the arbitrary whims of Xi or the Party bureaucracy. This is not the case. These new regulations are about serving the people and ensuring development is people-centered.

Where else do you hear of the concept of a “mortgage strike”? Imagine what would happen if such a thing happened in the West, especially the USA. How do you think the government would react when the banks started complaining about missed payments? You don’t have to imagine, let us take a look when a similar crisis happened in the USA, during 2008 - 2009.

The reason why so many people lost their homes during the 2008 financial crisis has to do with adjustable-rate mortgages (ARMs). In the US, ARM-dealing was highly predatory, promising very low interest to begin with, which would then greatly increase later on. People who took on such mortgages were planning to refinance their ARM later to avoid paying the higher interest rates, or planned to sell before then. But after the market collapsed, they were stuck in their ARM, lenders wouldn't allow refinancing. [30]

In China? It doesn’t work this way. Chinese interest rates are pegged to the loan prime rates set by the People's Bank of China, which during the “real estate crisis" has been carefully lowered [31]. Once US homeowners could not afford their higher mortgage payments, the banks foreclosed, repossessing their homes. But in China, instead of foreclosing, the PBOC has encouraged banks to allow the refinancing of mortgages, at the expense of profits. [32]

Thus, while private developers like Evergrande and Country Garden have suffered, Chinese homeowners’ mortgage rates have fallen to historic lows. The average default rate on residential mortgages has remained minuscule.

Central bank “independence” is praised by Western economists. The IMF typically forces it on peripheral countries as a structural adjustment condition. Once a victim country loses control over its own financial policy, it's helpless to end its underdevelopment. But in China, even talking about the possibility of central bank independence is not a good idea. Do that these days, and you can expect a visit from “Party discipline inspectors.” [33]

In response to the Real Estate crisis as well, Reuters reported that the government’s response to the crisis was to gradually nationalize the property market. Banks were allowed to extend credit to state-owned developers but instructed to steer clear of private real estate firms. [34]

State-owned enterprises are taking up a more important role in the property market. In 2022, SOEs accounted for around 40 percent of market share in terms of sales based on South China Morning Post estimates. With the previous number prior to this so-called demolition in 2021 being around a third or 33% of the market share. Sales performance is diverging across the sector. In the year to date, SOEs and quality developers like CR Land, Coli, Longfor Property and Yuexiu posted sales growth of between 70 per cent and 215 per cent year on year. In stark contrast, sales for troubled private developers like Times China, Sunac China and Zhongliang Holdings declined by 50 to 60 per cent year on year, owing to homebuyers’ reluctance to buy from them. [35]

However, by 2023, 89% of new land acquisitions will come from state-affiliated developers, helped by their stronger financing and sales capabilities. Because state-owned companies have more funding advantage, their share of the land market is expected to keep rising, and it will create more pressure for small- to mid-sized developers to acquire land (especially) in the core cities. [36]

Below is a chart from China Index Holdings to help you visualize it:

The left pie chart is in terms of monetary value, the right pie chart is in terms of firms.

In the chart, 10.7% of the monetary value of land acquisition in 2023, came from the private sector. 22.3% came from local SOE developers. 57.8% came from Central State Owned Enterprises. 9.2% came from joint-ventures. In terms of firm acquisition, 15% came from Private firms. 29% came from Central State-Owned Enterprises, with 51% coming from local SOE developers. And finally, 5% coming from joint ventures.

And more recently in 2024, the State reaffirmed that troubled private developers would be forced to default and fall to the wayside. The Government would not bail them out or assist them financially in any way. The government's priority is to ensure delivery of property projects, not to protect the business of property developers. [37]

A single sentence has caused such profound and positive changes for the citizens of the People’s Republic.

Healthcare Reforms

In the early 2000s, public hospitals used the 15% drug price-adding policy to increase hospital revenues, and doctors were motivated to prescribe high-priced and unnecessary drugs to patients. Consequently, patients and their families were overwhelmed by huge drug expenditures. Some were even pushed or back into poverty because of illness, which gradually aroused wide concern among the public and the government. [38]

Prior to Xi Jinping, there were, of course, efforts to remedy this issue. The National Reimbursement Drug List (NRDL) was first created in 2000 to improve access and reimbursement for hospital-purchased drugs. [39]

The NRDL was meant to be updated every 2 years, with thousands of national and provincial experts participating in a complex voting process. Due to the complex nature of the adjustment process and a lack of staff, it was only updated twice (2004 and 2009) before 2016 [40]. The long delay between NRDL updates meant that new drugs would experience significant delays between approval and reimbursement. From 2003 to 2013, there were 360 new drugs approved in China. However, only 76 (21%) entered the NRDL. [41]

Fiscal investment in healthcare in the PRC have more than tripled over the course of 2010 to 2018. In new drugs, pharmaceuticals from Pfizer to Roche have agreed to price cuts of as much as 70%. For generic drugs, prices have dropped an average of 52% so far through a government bulk-buying program. Funding for Chinese biotech firms has more than quadrupled within the span of 2017 to 2019. [42]

In 2016, the National Health Commission, National Development and Reform Commission, and the Ministry of Human Resources and Social Security initiated the first-round national-level drug price and NRDL access negotiation. By the new mechanism, the Chinese government can “cherry-pick” drugs and slash drug prices in exchange for reimbursement status. Finally, 3 drugs (gefitinib, icotinib, and tenofovir disoprox) out of 5 candidates successfully reached an agreement with the government, reducing their prices by 58.36% on average. [43]

In 2018, the National Healthcare Security Administration (NHSA) was established as a department to integrate the responsibility for the basic medical insurance and the price management of pharmaceuticals and medical services [44]. After its establishment, the NSHA initiated the 2018 round of negotiation, particularly for anticancer drugs. After 2 months of negotiation, 17 anticancer drugs entered the NRDL with an average price discount of about 56.7%, of which the highest was up to 70%.

Erbitux was one of the successfully negotiated medicines in this round, which is a targeted medicine for colorectal, neck and head. Before the agent was listed in the NRDL, patients could only purchase it at the original price, that is, 4,200 RMB a bottle. After negotiations, it fell to 1,295 RMB a bottle. [45]

From 2015 to 2023, the NRDL had an average of a 56% price reduction for pharmaceuticals, with a 77.7% successful negotiation rate. [46]

In 2022, 12 within-class anticancer drugs with 7 cancer diseases were analyzed, including 18 domestic (21 indications; 21 pivotal trials) and 18 imported (21 indications; 27 pivotal trials) novel anticancer drugs, respectively. The median monthly treatment price of domestic and imported drugs from the years of launch to 2022 had significantly decreased by 71% and 62%, respectively. Moreover, the median monthly treatment price of domestic targeted anticancer drugs on the market at launch ($3786 vs. $5393) and the latest ($1222 vs. $2077) was significantly lower than that of imported drugs. A 67.73% reduction and a 61.49% reduction, respectively. [47]

In 2021, Insulin VBP’s had a price cut of around 48.75% [48]. In 2022, Forty-two insulin products from 11 companies were procured, with a median price reduction of 42.08% [49].

According to the Legatum Institute, China is in the top 5 of the best healthcare systems in the world, being edged out by Taiwan, South Korea, Japan and Singapore in 2022. But we should not only look at drug procurement, we should also look at the People’s Republic of China’s response to the COVID-19 crisis.

As of May 31, 2021, a total of RMB ¥162.4 billion had been allocated by governments of all levels to fight the virus. The medical bills of 58,000 inpatients with confirmed infections had been settled by basic medical insurance, with a total expenditure of RMB ¥1.35 billion, or RMB ¥23,000 per person. The average cost for treating Covid-19 patients in severe condition surpassed RMB ¥150,000, and in some critical cases the individual cost exceeded RMB 1 million, all covered by the state [50]. The medical costs of the COVID-19 confirmed and suspected patients are mostly covered by the healthcare insurance and financial subsidy, and individuals do not need to pay. [51]

In terms of healthcare insurance, in 2020, about 95% of the population has at least basic health insurance coverage. A total of 25% of the people covered by the basic medical insurance participated in the employee medical insurance, a total of 344 million people; 75% participated in the residents' medical insurance, a total of 1.017 billion people. Medical assistance has subsidized 78 million poor people to participate in basic medical insurance, and the coverage of poor people has stabilized at over 99.9%. Maternity insurance coverage continues to expand. At the end of 2020, there were 235.673 million people participating in maternity insurance, and 11.669 million people enjoyed benefits. [52]

In 2014, the nominal reimbursement ratio of hospitalization was 85% in township hospitals, 70% in county hospitals, 55% in municipal hospitals and 50% in provincial hospitals. [53]

By 2020, China’s out of pocket health expenditure in total health expenditure fell from 59.5% in 2000 to 27.70% in 2020. Meaning that in 2020, 72.30% of health expenditure was covered by insurance. [54]

In short, we can see that the strides being made by Xi Jinping to reform and improve the healthcare system in China has had tangible effects on the increasing affordability of medical pharmaceuticals for the average citizen.

Wage Growth and Automation

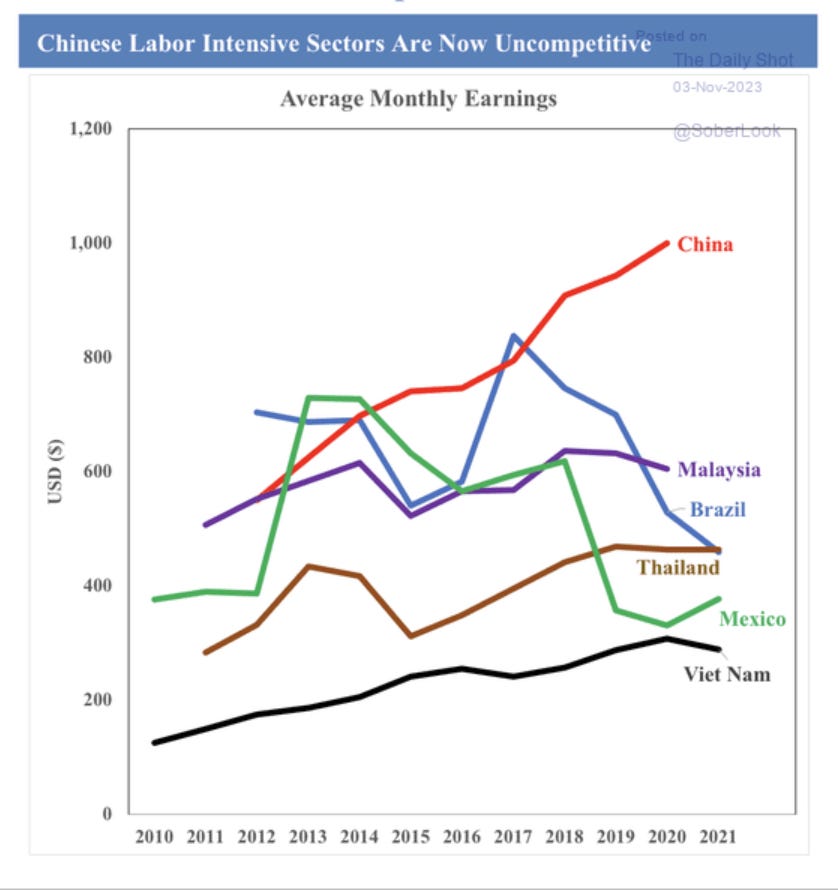

Over the course of 2013 to 2022, manufacturing wages have since doubled under Xi Jinping. Chinese laborers are paid on average of $8.29 USD an hour compared with Malaysian, Filipino, Vietnamese, Indian and Thai laborers who do not get paid more than $3 USD. [55]

China’s labor-intensive labor has not suffered a single wage decline in nominal terms from 2012 to 2021. Malaysia, Thailand, Brazil, Mexico and India has suffered at least one wage decline over the same period.

Interestingly, in 2016, Labor costs adjusted for productivity in China are only 4% cheaper than in the United States. In 2003, hourly compensation in the United States was 42 times higher than in China; the differential fell to nine times in 2009. Meaning over the course of 6 years, the wage gap between the USA and China declined by 4.66x per year. [57]

But if we don’t factor in productivity, in 2001, the Chinese wage gap between the USA was 30 times, by 2016 though, it had fallen to 6.5 times. And by 2021, it had shrunk to 3.5 times. So, over the course of 21 years, the gap between the USA and China declined by 1.26x per year. [58]

Many pundits may claim this rise in wages is making China “uncompetitive” and will reduce China’s labor productivity. However, one should refer back to both the 1990s and 1920s — our modern benchmarks for productivity success stories — an earlier period of rapid productivity growth and technological change. Economist Gavin Wright considers the adoption of two general-purpose technologies: electricity in the ‘20s and computers in the ‘90s. Both had existed for some time but weren’t widely adopted until rising labor costs provided the right incentives. He observes that in both periods strong wage growth started before productivity accelerated. [59]

In this context, it would be the 4th industrial revolution, with the adoption of AI and increasing automation that will be adopted in this spur for wage growth. If Wright is correct, this rise in wages will cause a spur in demand for more and more enterprises to adopt automation. Empirically, we can see at the very least, there has been trending automation since 2013.

In 2014, Xi Jinping said:

“Seeing this, I was thinking that our country will become the largest market for robots, but can our technology and manufacturing capabilities cope with this competition? We must not only improve the level of our country's robots, but also occupy as many markets as possible. There are still many such new technologies and new fields. We must assess the situation, consider the situation comprehensively, plan quickly, and make solid progress.” [60]

In 2017, China ranked 20th out of a list of robot density per 10,000 workers. Only having just under 100 robots per 10,000 workers. [61]

In 2021, China had installed 18 percent more robots per manufacturing worker than did the United States. And when controlling for the fact that Chinese manufacturing wages were lower than U.S. wages, in 2021, China had 12 times the rate of robot use in manufacturing than did the United States. [62]

China’s growth rate in terms of robotics from 2017 to 2021 far outstrips any country on the list. China’s automation rate during those few years increased 3-fold over, higher than any other countries rate of growth.

By 2022, China had the 5th highest robot density in manufacturing per 10,000 workers. While Chinese robots generally do not match the quality of the best Western companies, many Chinese robots are 80% as good as the best foreign European ones but are much cheaper by around 30%. [62]

When we compare robot adoption rates as a share of the adoption rates that would be expected based on countries’ manufacturing wage levels, we can see that China leads the world with an astounding 12.5 times more robots adopted than would be expected, up from 1.6 times more in 2017. [62]

China’s rapid adoption of automation and wage increase is an unprecedented scale of growth, which will naturally accelerate China’s productivity to higher heights. Xi Jinping’s mandate of rapidly developing automation and robotics will reap great fruits for the Chinese nation.

Conclusion

In short, Xi Jinping Thought has caused sweeping changes across the broad Chinese political and economic scene: cracking down on financial speculation and driving forward with rapid productivity gains via automation and wage increases. The great clearsighted and ever-correct Xi Jinping Thought drives forward immense positive quantitative and qualitative changes in the People’s Republic of China, by faithfully adhering to the Communist Party of China’s philosophy of “Serving the People” and following the principle of People-Centered Development.

Bibliography

[1] Xi says China's reform enters deep-water zone, Global Times.

[2] A New Starting Point for China's Development: A New Blueprint for Global Growth

[5] The Central Party History Research Office explains Xi Jinping’s two statements that cannot be denied

[6] Correctly Deal With Both Historical Periods Before and After Reform and Opening Up

[7] Mao Zedong Thought vs Socialism with Chinese Characteristics (Summary 107)

[8] Law of the People's Republic of China on Farmers' Professional Cooperatives

[10] China New Observation|The “return” of supply and marketing cooperatives?

[12] Average number of people living in households in China from 1990 to 2022, Statista.

[13] Number of employed people in China from 2013 to 2023, Statista.

[14] Xi Focus: Xi stresses deepening reforms of supply and marketing cooperatives, Xinhua.

[16] Welcome to apply for the All-China Federation of Supply and Marketing Cooperatives

[17] What do supply and marketing cooperatives do now?

[20] More than 98% of agricultural business entities across the country are still small farmers.

[21] Houses are for living in, not for speculation

[22] Developers Face New Debt Limits as Property Crackdown Continues

[23] China’s Plan to Manage Evergrande: Take It Apart, Slowly

[24] Mortgage strikes threaten China’s economic and political stability

[25] Analysis: China's mortgage boycott quietly regroups as construction idles

[26] China Weighs Mortgage Grace Period to Appease Angry Homebuyers

[28] Is China’s housing market in trouble?

[29] China Puts Money Behind Singapore Model in Major Housing Shift

[30] Most broker customers couldn't refinance: poll

[31] China cuts key interest rate as recovery falters

[32] Chinese Banks and RMBS Could See Minor Impact from Push to Lower Mortgage Rates

[33] Beijing Reins In China’s Central Bank

[34] China property market faces more nationalisation

[35] State-owned firms to extend domination of China property market, support its recovery, analysts say

[36] China's state-owned developers dominate sales, land markets in 2023 - surveys

[37] Beijing says property developers in deep trouble must go bankrupt

[38] Retrospect of the policy of drug price addition in hospitals and its influences - M Zhang, Y Bian - Chin Health Serv Manage, 2007

[39] Guan X, Liang H, Xue Y, Shi L.An analysis of China's national essential medicines policy. J Public Health Policy. 2011;32(3):305-319

[40] Zhou Q, Chen X-Y, Yang Z-M, Wu YL.The changing landscape of clinical trial and approval processes in China. Nat Rev Clin Oncol. 2017;14(9):577-583.

[41] Mossialos WHO, Ge E, Hu Y, Wang J, L.Pharmaceutical Policy in China: Challenges and Opportunities for Reform. World Health Organization. Regional Office for Europe; 2016.

[42] China Is Striving for the World’s Best, Cheapest Healthcare

[43] China to cut prices of expensive patent drugs

[44] Xu J, Jian W, Zhu K, Kwon S, Fang H.Reforming public hospital financing in China: progress and challenges. BMJ. 2019;365:l4015.

[45] 17 cancer drugs added to insurance program list

[46] China Starts Implementing the 2023 National Reimbursement Drug List (NRDL)

[48] China's Insulin VBP Sees Average Price Cut of 48.75%

[50] Full Text: Fighting COVID-19: China in Action

[52] Questions and Answers on the “14th Five-Year Plan” National Medical Security Plan

[55] Global firms are eyeing Asian alternatives to Chinese manufacturing

[56] Global firms are eyeing Asian alternatives to Chinese manufacturing

[57] Making it in China is not the bargain it used to be, new study reveals

[58] The East-West Wage Gap Not Nearly As Compelling As It Once Was

[59] Productivity Growth and the American Labour Market: the 1990s in historical perspective