State Ownership and the People’s Republic

Investigating State Ownership in China's Economy Today

The dawn of the twentieth century saw the rise of modern, planned national economies around the world. In many of these cases, planned economies often were coupled with state ownership of production. China, especially due to becoming a Marxist-Leninist state in 1949, is no exception to this trend. It is commonly misconceived by both leftists and rightists that the People’s Republic of China has ceased to plan its economy; that the government has relinquished its obligations of maintaining state control, the private sector and “adopted capitalism”.

When it comes to analyzing how state ownership operates within the People’s Republic of China, the information that is available on the Western internet tends to be sparse and vague. Many sources do not give specific evidence of how State-Owned Enterprises (SOEs) function, nor do they elaborate just how widely proliferated SOEs are, formally or otherwise. This article is designed to clarify the way SOEs and their subsidiaries function and interact with China’s domestic economy today.

Formal State Ownership

“State-owned enterprises are an important material and political foundation for socialism with Chinese characteristics, and an important pillar and reliance for the party to govern and rejuvenate the country.”

— Xi Jinping, General Secretary of the Communist Party of China

It is a well-established fact within Chinese political discourse that state-owned enterprises are an ever-present fact of the Chinese economy that won’t simply just “vanish” overnight or “erode” over time. In fact, since Reform and Opening Up, while the overall quantity of state-owned enterprises has gone down, the overall quality has increased.

Rather than going on the path of root-and-branch privatization, the government has instead sought to make the numerous state-owned enterprises that still remain as efficient and competitive as possible. As a result, the top 150 SOEs, far from being inefficient, have instead become enormously profitable, the aggregate total of their profits reaching $150 billion in 2007. Unlike in the West or Western-aligned states, where privately owned firms overwhelmingly predominate, most of China’s best-performing companies are to be found in the state sector. [1]

Contrary to popular belief regarding “Communism”, profit and to make a return on one’s investment is not contradictory to the way state-controlled firms should be run. In fact, it would be damaging if these firms were run in a way where they were actively making a loss or were wasting resources.

Contribution to GDP and Scale of Assets

In 2011, it was found that roughly 50% of non-agricultural GDP was generated by SOEs. Similarly, in regard to economic industries/sectors in which SOEs play a dominant or majority role, those include defense, electric power, petroleum and petrochemicals, telecommunications, coal, civil aviation, and shipping; as well as equipment manufacturing, automobiles, information technology, construction, iron and steel, nonferrous metals and chemicals. [2]

In 2017, that number stood at 63.6%, where China’s GDP was RMB ¥82 trillion, of which non-financial SOEs count for RMB ¥52.2 trillion [3]. In 2021, SOEs accounted for around 66% of China’s GDP [4]. So, even formally speaking, in terms of overall contribution to GDP, SOEs have played a significant amount, rising over the past 10 years from 50% to 66%, rising approximately 1.6% to their contribution to GDP per year. In 2023, that number climbed to 68% of China’s GDP: China’s GDP was RMB ¥126 trillion, of which non-financial SOEs accounted for RMB ¥85.7 trillion. [

From 2002-2011, the value of SOE assets as a percentage of GDP started at roughly 550% before declining to a rate of roughly to 430% by 2008, its lowest point, before reaching a plateau of around 450% since 2009.

Note, when Western analysts measure state-owned enterprises, they tend to only factor in what is directly translated as 国有企业, which is formally classified as a non-financial state-owned enterprise. Typically, when comparisons are made from Western studies or articles, they only focus on “SOEs” but neglect the two other formal “SOE categories” which are financial SOEs (国有金融/中央金融企业) and administrative SOE assets (行政事业性国有资产).

This is why estimations for “SOE value” may be lost in translations and only partially accurate results can be extrapolated. For the following two sources, one produced by the IMF and the other produced by WSJ, the operative Chinese “SOEs” will be referred to as non-financial SOEs for clarification. Non-Chinese SOEs elsewhere in the world don’t follow these three distinctions.

In 2018, a study from the IMF found that Non-financial SOEs assets for China as a % of GDP amounted to 180% of GDP. While in 2015, Italy, India, South Korea, Saudi Arabia and Norway’s SOEs did not rise above 50% [6]. According to WSJ, the value of French SOE assets in 2008 as a % of GDP amounted to 686 billion USD, which is 28% of GDP. In the same year, Chinese Non-financial SOEs were 6 trillion USD, or 133% of GDP [7].

In 2010, 94% of all assets held by the top 150 companies were controlled by the state, which represented 41.2% of all corporate assets in China, out of the total of roughly 5 million registered companies [8]. In 2012, the total assets held by the State sector in China amounted to 55.78% or 53% depending on the estimate used [9]. However, in comparison with European nations during the same year (elaborated by the figure below), the total assets of Eastern European nations (largely former Eastern Bloc) held by the state sector were around 13%. For the Netherlands, Italy, Spain, France, Belgium and Portugal, it was around 4.60%. For Ireland and the UK, even less than that number. For Austria and Germany, around 10.79%. For Scandinavia, it was 6.02%. [10]

In 2022, the total value of SOE assets as a percentage of GDP amounted to 608%, of which ¥109.4 trillion or 90.4% of GDP was held by all 97 Central State Owned Enterprises (CSOEs), controlled directly by the SASAC (more on that later). And non-financial SOEs held 339.5 trillion, which accounts for 280.5% of GDP [11]. In comparison to the largest 500 private enterprises in the same year, their amassed assets held ¥41.64 trillion RMB, of which represents only 34.4% of GDP, which is dwarfed by the amount held by the 97 CSOEs [12]. In regard to share of total assets, SOEs own 60% of China's total assets as of 2021 [13]. Note, RMB (Renminbi) is more commonly known as Chinese Yuan (¥). Second note, a CSOE is an SOE directly controlled by the Central Government.

In 2019 there were 3,777 listed companies on the public stock exchanges in Shanghai and Shenzhen, of which you need an operating income of ¥100 million RMB per year to even be available for listing, cumulative over the course of 3 years. Out of total assets, SOEs held 98% in the Telecommunications sector, 95% in the airline sector, 94% in the infrastructure sector and more than 93% in the utilities and energy sector. In the industry sector 74%, in the materials sector, more than 63% and in automobiles, more than 62%. [14]

In 2023, out of a total of 4,763 listed companies, of which 1,300 are formally classified as SOEs. They make up 27% of the total enterprises, but capture 69% of the market revenue and 77% of the total profits. Most leading listed companies across key industries, including but not limited to banks, insurance, brokerage, oil & gas, chemicals, coal, power, telecom, construction, Chinese medicine and liquor, are all SOEs. [15]

Furthermore, the amount of private involvement is exaggerated. As of the end of 2017, there are only 17 private-owned banks among 4,532 financial institutions classified as the banking industry. The number of people employed by these 17 private-owned banks only accounts for 0.1% of all banking staff. For example, in 1997, POEs (Privately Owned Enterprises) in the industrial sector accounted for only 6.5% by number, and this figure has increased to 57.7% in 2017. However in 2000, POEs in the industrial sector accounted for only 3.1% by the size of assets, and this figure peaked at around 22% in 2013, stagnating to a slight decline by 2017 of 21.6%. [16]

Examples of Dominant SOEs

Now that the persistence of SOEs in the modern Chinese economy has been established via statistical evidence, I want to provide some empirical evidence, some examples that could be used or shared in future for reference. Circling back to the point about “key sectors” of which SOEs must dominate, below are a few examples of the following SOEs that dominate their respective key sectors.

The power-generating industry in China is dominated by five SOE power-generating company groups: China Huaneng Power Group, China Datang Corporation, China Huadian Corporation, China Guodian Corporation, and China Power Investment Corporation. And the public utilities sector is dominated by the State Grid Corporation of China (SGCC) and China Southern Power Grid Corporation [17]. The telecommunications industry in China is dominated by three SOE telecommunications carriers: China Telecom, China Unicom, and China Mobile [18].

The petrochemicals industry is dominated by five SOE company groups: China National Petroleum Corporation, Sinopec, Sinochem, China National Offshore Oil Corporation and Shandong Energy [19]. And the natural gas industry is dominated by five SOEs as well, Sinopec, CNPC, CNOOC, Beijing Enterprises Group and Shenenergy Group [20].

China Baowu Steel Group Corporation, produces 80% of the auto-sheet metal for use in automobiles, major appliances, airplane fuselages and wings, architecture, and others and 60% of the silicon steel which are used in generators, motors, and transformers. Baowu steel remains to be a global leader in both categories as of 2022 [21].

The world’s largest producer of rolling stock and locomotives is under one company, the China Railway Rolling Stock Corporation — which is a CSOE — has 90% of the market share for train production [22]. The largest ship producer domestically and worldwide and sole ship producer in China, the Chinese State Shipbuilding Corporation produces 48% of all ships in the world [23].

You have China Minmetals, which has 90% of the domestic metallurgical market share [24]. They also hold 90% of the contract value for domestic metallurgical engineering and construction, which is the construction of industrial metal production engineering machines and items [25].

These are just a few of the prominent examples of the large and dominant SOEs that permeate through China’s domestic market. The more upstream an economic sector is, the more state ownership it will have. This is the general rule of thumb for the state involvement within the domestic economy.

The Shareholder System

The State-owned Assets Supervision and Administration Commission of the State Council (SASAC) is an institution directly under the management of the State Council. It is an ad-hoc ministerial-level organization directly subordinated to the State Council. The Party Committee of SASAC performs the responsibilities mandated by the Central Committee of the Chinese Communist Party. [26]

The way ownership is substantiated or demonstrated is through stock ownership. The SASAC owns 100% of the stock of a total of 98 CSOEs. There is a common misconception that companies must be 50% or more, or somehow totally state owned to be in function “state owned” or operate according to party directives. On paper, SOE employment rates and output rates are formally lower than the non-state sector, yet they continue to persist and play a dominant role in the economy.

How is this possible? Through the shareholder system. One way the CPC maintains functional control over multiple enterprises is through a diverse shareholder system, where one CSOE directly or indirectly controls 100s or 200 enterprises via their own subsidiary system. Lenin notes in his book, Imperialism, the Highest Stage of Capitalism of precisely this phenomenon, although inverted as it is now the state who is the “shareholder”, while he was analyzing the bourgeoisie who were shareholders.

The head of the concern controls the principal company (literally: the “mother company”); the latter reigns over the subsidiary companies (“daughter companies”) which in their turn control still other subsidiaries (“grandchild companies”), etc. In this way, it is possible with a comparatively small capital to dominate immense spheres of production. Indeed, if holding 50 per cent of the capital is always sufficient to control a company, the head of the concern needs only one million to control eight million in the second subsidiaries. And if this ‘interlocking’ is extended, it is possible with one million to control sixteen million, thirty-two million, etc… As a matter of fact, experience shows that it is sufficient to own 40 percent of the shares of a company in order to direct its affairs, since in practice a certain number of small, scattered shareholders find it impossible to attend general meetings, etc. The “democratization” of the ownership of shares, from which the bourgeois sophists and opportunist so-called “Social-Democrats” expect (or say that they expect) the “democratization of capital,” the strengthening of the role and significance of small scale production, etc., is, in fact, one of the ways of increasing the power of the financial oligarchy.” [27]

Lenin understood that it was entirely possible for the shareholding system to “increase the power” of the financial oligarchy. But what if, instead of a financial oligarchy sitting at the top of the pillar, it is the Communist Party? Or more specifically, the SASAC.

Lenin notes in the above quote that owning merely 40% of the shares of a single company is sufficient to direct its affairs. And how “Mother companies” reign supreme over “Daughter companies” and indirectly control “grandchildren” companies. Therefore, it is entirely possible for “1 million to rule over 32 million”. And this is precisely how the SOEs obfuscate their formal state ownership within the Chinese economy while still maintaining de facto control and influence.

This phenomenon is noted by Derrick Scissors, who is a former Senior Research Fellow at The Heritage Foundation. In 2007, he found that while 100% of state ownership may be “diluted” by division of ownership into different shareholders, of which are non-state, the majority of ownership/controlling shareholder largely trended towards state ownership. This is despite the fact that they might formally be considered non-state owned or sometimes foreign media may even label them private. He says that however, this phenomenon does nothing to change state control. Despite them being listed on foreign stock exchanges, the ultimate control rights remain in the hands of the state. [28]

No matter their shareholding structure, all national corporations in the sectors that make up the core of the Chinese economy are required by law to be owned or controlled by the state. These sectors include power generation and distribution; oil, coal, petrochemicals, and natural gas; telecommunications; armaments; Aviation and shipping; machinery and automobile production; information technologies; construction; and the production of iron, steel, and nonferrous metals. The railroads, grain distribution, and insurance are also dominated by the state, even if no official edict says so. [28]

The same is noted by Margaret Pearson who argues that despite the issuing of stocks, these stock issuances are not used for the purpose of wholesale “denationalization” or “privatization” of enterprises, but the intended goal is to rather upgrade and enhance the value of corporate state-owned assets. Even though some firms may have been listed on the stock market, their parent firms or “Mother firms” control rights firmly remain in the hands of the state. [29]

Stephen Green, a member of the Royal Institute of International Affairs continues to corroborate the claim, making the statement that the way stocks are issued is not for the sake of denationalization of industries, but to support and subsidize SOE restructuring and to prevent private companies from raising capital. [30]

A research study in 2009 concluded that the “privatization” campaign of China drastically differs from the ones conducted in Eastern Europe, that the sale of shares do not fundamentally alter state control. And that in fact, there has been no meaningful transfer of state control over to private hands. The majority of companies in China have around 66% of their shares being held in state hands. Even if shares can be traded/floated on the market, for the most part, shares will still indefinitely be maintained by state actors. [31]

In 2014, another study found that China’s domestic market is entirely state dominated. The central government plays every role from issuer, to underwriter, to regulator, to controlling investor and manager of the exchanges. Efforts to simplify domestic arrangements have served only to conceal the fact that the state in its many guises still owns nearly two-thirds of domestically listed company shares. The combination of state monopolies with “Wall Street expertise” and international capital has led to the creation of national companies that represent little more than the incorporation of China's old Soviet-style industrial ministries. [32]

A 2017 research paper finds that the state appointed nomenklatura working within these large “mother” companies are responsive primarily to the directives of the state instead of minority shareholders within their “daughter” or “granddaughter” firms. The core holding company is the one that coordinates business activity of the “daughter” and “granddaughters”, and these core holding companies are always dominated by state ownership. These business activities are committed in the interest, above all, of state industrial policy, and certainly with a preference for such national policy over what might be in the interest of shareholder wealth maximization for the nongroup, minority shareholders invested in the individual legal person subsidiaries often through the public capital markets. [33]

From 1990 to 2003, it was found that only around 7% of all listed firms could truly be considered “private”. These companies are allowed to have access to private revenue, but their control rights are strongly within the hands of the state and should therefore be considered state firms. Even though many of these firms are not formally listed as SOEs, they are rather considered to be either joint-venture or shareholding firms instead. [34]

LLCs/Shareholding Firms

Widespread “privatizations” of small SOEs reduced the total number of SOEs from 250,000 in 1995, to 127,000 in 2005. It is naïve to view the state as simply having divested itself from ownership of the state sector. Virtually all of the figures that scholars and the popular press have picked as evidence of the declining role of the state, relates to the decline in state shares but ignores the rise of institutional shares. [35]

The transformation of SOEs into share-holding firms took several forms: shareholding cooperatives, jointly owned enterprises, limited liability corporations and limited shareholding corporations. These firms held over 50% of capital assets and generated 35% of national sales. They replaced SOEs as the dominant public sector employers in the interior of the country. These hybrid forms were supposed to operate under hard budget constraints. [35]

The introduction of stock markets in China appeared to be a capitulation towards “capitalism”. However, in July 2015, a crisis in the stock market revealed the inner contradictions between market pressures and state control as it exposed peculiar features of China's markets. Formally, all the institutions, organizations, administrative and legislative forms that are required to replicate Western stock markets exist. However, all aspects of the capital markets remain owned by some agency of the state. As a consequence, when share prices began to collapse in July 2015, state banks were told to lend US $209bn to the wholly state-owned China's 89 Securities Finance Corp in order to buy stocks. Market volatility was thereby contained by massive state intervention. This means that the fate of listed companies are ultimately determined by budget constraints which are set by the Central Government. [35]

The widespread underestimation of the influence of state ownership in the economy is not simply a question of misidentifying concealed public ownership relations, but also of understanding the ‘dynamics of control’ exercised by organs of the party and state. [36]

There is a consistent problem when attempting to identify firms as “state owned”. Many times, functionally state owned firms are listed as “foreign-held” simply because 30% of its shares are owned by a foreign entity, despite the control rights being operated by the state. [37]

For example, the joint ventures of the Shanghai local government with GM and Volkswagen (Shanghai-GM and Shanghai-VW) are registered as foreign companies, despite the fact that the Shanghai local government holds 50% of each company (Of which is the largest share in the case of Shanghai-VW). [37]

This can also happen when the company is owned by a holding company registered outside of mainland China. For example, Lenovo and CNOOC (a state-owned oil company) are owned by holding companies registered in Hong Kong and, thus, legally registered as foreign owned in China. Despite the control rights firmly being managed by state hands. [37]

Second, many state-owned companies, particularly after 1998, are registered as limited-liability or publicly traded companies, despite the controlling stake held by a state-controlled holding company. The Baoshan steel company and Shanghais SAIC Group’s stand-alone car company (SAIC) discussed earlier are examples of publicly listed companies and, thus, registered as share-holding companies but with a controlling stake held by a holding company owned by the Chinese state. [37]

66% of all firms are directly or indirectly owned by the SASAC. In 2012, the number of “underreported” state firms ran at 50%, of which were being registered as private firms. Meaning that the formal state share of the economy is actually 50% larger. Note, state ownership being defined here as 50% or more of a firm being owned by the state. [37]

We can extrapolate that number and apply it to asset ownership in 2012, of which 53% of all assets in China were held by the State Sector. Let’s again assume that the state having at least 50% ownership makes a company state-owned. 50% of 53 is 26.5, meaning that in 2012, if we include the "underreported" sector of the state, this means that the total state ownership of assets in 2012 actually amounts to 79.5%.

Examples of the Shareholder/LLC system at work

An example of how this works in function will be demonstrated using the example of the company known as Sinopec: a petrochemicals company owned directly by the SASAC and is one of the largest if not the largest petrochemicals company in the world. Sinopec has a monopoly on all downstream hydrocarbons businesses in China. [33]

A sinopec core company which is 100% wholly owned by the SASAC is the center of the Sinopec group. A majority-controlled subsidiary, department, or affiliated entity would function as a dedicated "finance holding company" necessary for the allocation of funds and finance to and among operations and entities included in the Sinopec Group. Sinopec Group Holding Company - explicitly permitted in its business license to invest in other entities - in turn owns a vast number of only Sinopec business-related subsidiaries, each with a business scope allowing it to operate in a defined sector within the group's larger monopoly or defined geographical areas.

A majority-controlled subsidiary, department, or affiliated entity would function as a dedicated "finance holding company" necessary for the allocation of funds and finance to and among operations and entities included in the Sinopec Group. Sinopec Group Holding Company, explicitly permitted in its business license to invest in other entities, in turn owns a vast number of only Sinopec business-related subsidiaries, each with a business scope allowing it to operate in a defined sector within the group's larger monopoly or defined geographical areas.

Those subsidiaries will always show majority equity ownership in the hands of the Sinopec Group Holding Company or one of its controlled subsidiaries, but they can be financed directly by bank loans, minority non-public investment, or the public shareholder markets, domestic or foreign. This Sinopec Group can seek to reorganize a traditional SOE grouping of productive and social assets conducting a petrochemicals business, like in the Shanghai suburbs of Jinshan District into a Sinopec Group Holding Company-controlled company called "Sinopec Shanghai Petrochemical Company Limited," which could complete an initial public offering on the PRC domestic or foreign shareholder markets.

After the IPO, issuer Sinopec Shanghai Petrochemical Company Limited would still be dominated absolutely by the core holding company (which is the Party-State Ran State-Owned Enterprise of Sinopec) via an 80 percent equity stake and its power to appoint all directors and officers of the listed subsidiary.

This is how Sinopec controls over hundreds of its own subsidiaries even though a lot of them aren’t formally “owned” or listed as SOEs according to official Chinese statistics.

An example of how a “foreign listed” company is actually state owned would be the SMIC, otherwise known as the Semiconductor Manufacturing International Corporation. The only reason it is considered “foreign listed/foreign owned” is because 58% of its shares are listed on the Hong Kong stock exchange.

14.11% of its shares are held by Datang HK which is a wholly-owned subsidiary of Datang Holdings, which in turn is wholly-owned by CICT which is a central state owned enterprises. [38] CICT itself directly holds an additional 0.92% of the total shares, bringing the total amount to 15.03%. 7.80% of shares are held by Xinxin HK, a wholly-owned subsidiary of Xunxin (Shanghai) Investment Co., Ltd., which in turn is wholly-owned by China IC Fund which is a state owned investment fund. An additional 1.61% is held directly by the IC fund. 0.46% is held by Guoxin investment which is a state owned fund. 0.50% is held by a subsidiary of the China construction bank which is a state owned bank. Finally, another 0.43% is held by a subsidiary of the Chinese merchant bank which is a state owned bank as well.

The total amount of state ownership amounts to 25.83% [39]. The HKSCC share refers to just shares/stock listed on the Hong Kong stock exchange, which does not accurately reflect controlling shares. These shares can be bought by anyone who has access to the Hong Kong stock market. The majority shareholder and the largest shareholders are all state owned enterprises, which are either directly or indirectly connected to the central government with varying layers of connection. Even though the SMIC is not “formally state owned” it is functionally state owned.

Another even simpler example would be the Mcdonald's China franchise, even though on paper it is a foreign enterprise, bearing the company name/franchise name of “Mcdonald”. The controlling shareholder is a SOE known as CITIC, which holds 52% of the total shares. Making Mcdonalds in China functionally state owned despite being formally a foreign owned company. [40]

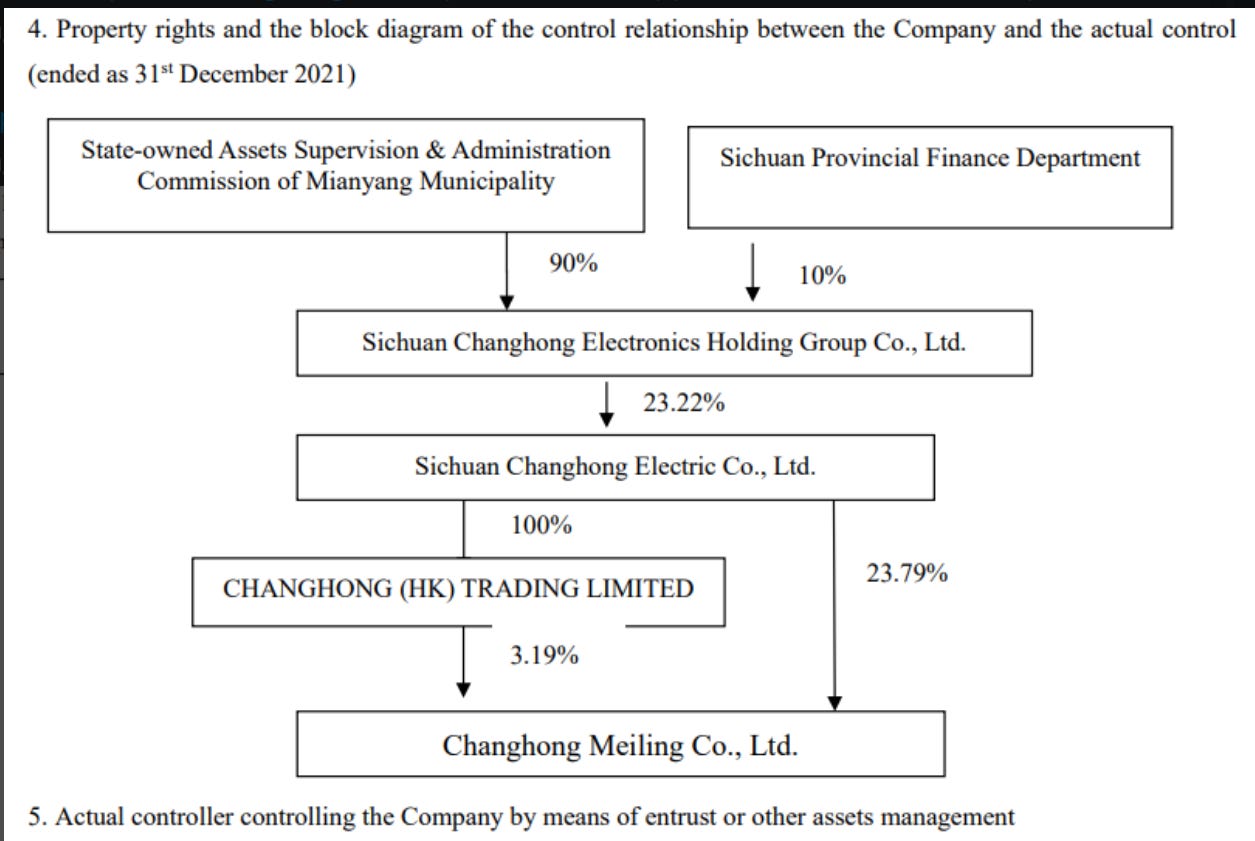

Finally, the last example demonstrates how an LLC can still functionally be a state-owned company even though the formal designation is of a “limited liability company”. Sichuan Changhong Electric is China’s largest television producer and the sole producer of batteries for the Chengdu J-10 “Vigorous Dragon”, a multirole combat aircraft. Even their official shareholders report states the following:

Sichuan Changhong Electronic Co., Limited (“Sichuan Changhong”), a company incorporated in the PRC with its shares listed on the Shanghai Stock Exchange, has obtained the control over the board of directors of the Company since 2012. Sichuan Changhong Electronics Holding Group Co., Ltd., (“Sichuan Changhong Holding”, a company established in the PRC and wholly-owned by the State-owned Assets Supervision and Administration Commission of the Mianyang city government and one of the Controlling Shareholders) is the single largest shareholder of Sichuan Changhong, which held approximately 23.22% of the entire issued share capital of Sichuan Changhong and has de facto control over the composition of the majority of the board of Sichuan Changhong. [41]

Below is a chart that goes over the overall ownership structure that makes it easier to visualize.

Conclusion

In conclusion, “formal” SOE ownership is deliberately obfuscated and downplayed by Western media despite the large impactful role it continues to play within the Chinese domestic economy. Similarly, “informal” SOE ownership via LLCs, shareholding companies and joint-ventures with foreign enterprises have caused them to be counted as “non-SOEs” despite functionally acting upon state directives. SOEs continue to persist within China’s economy and continue to actively grow in size, scale and scope of economic activities.

References

Formal State Ownership

[1] Jacques, Martin. 2012. When China Rules the World. p. 184.

Contribution to GDP and Scale of Assets

[2] Szamosszegi, Andrew, and Cole Kyle. 2011. An Analysis of State-Owned Enterprises and State Capitalism in China. p. 1. https://www.uscc.gov/sites/default/files/Research/10_26_11_CapitalTradeSOEStudy.pdf.

[3] Latest Lessons in Bankruptcy of State-Owned Enterprises (SOEs) in China: An interactive structural approach model (ISM) approach. https://www.hindawi.com/journals/ddns/2022/1109442/.

[4] State-Owned Enterprises’ Responses to China’s Carbon Neutrality Goals and Implications for Foreign Investors.

https://gjia.georgetown.edu/2023/02/15/state-owned-enterprises-responses-to-chinas-carbon-neutrality-goals-and-implications-for-foreign-investors/.

[42] Economic performance of state-owned and state-holding enterprises nationwide from January to December 2023, Ministry of Finance of the People’s Republic of China.

https://zcgls.mof.gov.cn/qiyeyunxingdongtai/202401/t20240129_3927581.htm.

[5] Rise of the ‘shareholding state’: financialization of economic management in China | Socio-Economic Review | Oxford Academic.

https://academic.oup.com/ser/article-abstract/13/3/603/1670234.

[6] People’s Republic of China: Selected Issues, Volume 2021, Issue 012, IMF.

https://www.elibrary.imf.org/view/journals/002/2021/012/article-A002-en.xml.

[7] China's 'State Capitalism' Sparks a Global Backlash, WSJ. https://www.wsj.com/articles/SB10001424052748703514904575602731006315198.

[8] Khoo, Heiko. 2018. Is China still socialist? A Marxist critique of János Kornai’s analysis of China. p. 85-89.

https://kclpure.kcl.ac.uk/ws/portalfiles/portal/136790902/2018_Khoo_Heiko_1068757_ethesis.pdf.

[9] Pei, Changhong, Chunxue Yang, and Xinming Yang. 2019. The Basic Economic System of China. p. 24-25.

[10] State-Owned Enterprises Across Europe: Stylized Facts from a Large Firm-Level Dataset. p. 17.

https://kclpure.kcl.ac.uk/ws/portalfiles/portal/136790902/2018_Khoo_Heiko_1068757_ethesis.pdf.

[11] Comprehensive report of the State Council on the management of state-owned assets in 2022.

https://mp.weixin.qq.com/s/nvBGqtx7MuPB8RTC9XT6jA.

[12] The top 500 Chinese private enterprises in 2022 released a total operating income of 38.32 trillion yuan.

https://www.xinhuanet.com/energy/20220907/79f0e58b387f4e7c903a51be2a8fc3b6/c.html.

[13] SOE reforms key to smooth recovery, ChinaDaily.

https://archive.ph/44ZmP#selection-403.68-403.79.

[14] García-Herrero, Alicia, and Gary Ng. 2021. China’s State-Owned Enterprises and Competitive Neutrality. p. 10. https://www.bruegel.org/sites/default/files/wp-content/uploads/2021/02/PC-05-2021.pdf.

[15] China SOEs – the journey to extract values from their re-rating and revaluation trajectory from Premia Partners.

https://archive.ph/mMjIq#selection-233.0-236.0.

[16] Liu, Kerry. 2021. The Rise and Fall of China’s Private Sector: Determinants and Policy Implications. p. 8.

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3921568.

Examples of Dominant SOEs

[17] Lewis, Joanna I. 2023. Cooperating for the Climate: Learning from International Partnerships in China's Clean Energy Sector. MIT Press. p. 44.

[18] Telecommunications industry in China, Statista.

https://www.statista.com/topics/6577/telecommunications-industry-in-china/#topicOverview.

[19] The 5 Biggest Chinese Oil Companies, Investopedia.

https://archive.ph/3POHm#selection-2275.1-2275.36.

[20] Top 5 Chinese Natural Gas Companies, Investopedia.

https://www.investopedia.com/articles/markets/090315/5-biggest-chinese-natural-gas-companies.asp.

[21] China Baowu Steel Group Corporation Limited, FitchRatings.

https://www.fitchratings.com/research/corporate-finance/china-baowu-steel-group-corporation-limited-09-03-2022.

[22] Chinese rolling stock manufacturers merge to form CRRC Corp, Railway Gazette International.

https://www.railwaygazette.com/business/chinese-rolling-stock-manufacturers-merge-to-form-crrc-corp/40956.article.

[23] China becoming world’s go-to for shipbuilding after ‘boom of overseas orders’, but global de-risking threatens to rock the boat, South China Morning Post.

https://www.scmp.com/economy/global-economy/article/3225973/china-becoming-worlds-go-shipbuilding-after-boom-overseas-orders-global-de-risking-threatens-rock.

[24] Minmetals Holding Corporation, Publication of Offering Circular. p. 14.

https://www1.hkexnews.hk/listedco/listconews/sehk/2021/0421/2021042100263.pdf.

[25] China Minmetals Corporation, FitchRatings.

https://www.fitchratings.com/research/corporate-finance/china-minmetals-corporation-16-08-2021.

The Shareholder System

[26] About Us, SASAC.

http://en.sasac.gov.cn/aboutus.html

[27] Lenin, Vladimir. 1917. “III. Finance Capital and the Financial Oligarchy.” In Imperialism, the Highest Stage of Capitalism. Marxists.org. https://www.marxists.org/archive/lenin/works/1916/imp-hsc/ch03.htm.

[28] Liberalization in Reverse, Heritage Foundation.

https://www.heritage.org/global-politics/commentary/liberalization-reverse.

[29] Pearson, Margaret. 2005. “The Business of Governing Business in China: Institutions and Norms of the Emerging Regulatory State.” p. 304. https://www.jstor.org/stable/25054295.

[30] Non-performing, The Economist.

https://archive.ph/B5kSb#selection-863.68-863.133.

[31] Yeung, Horace. 2009. “Non-Tradable Share Reform in China: Marching towards the Berle and Means Corporation?” https://digitalcommons.osgoode.yorku.ca/cgi/viewcontent.cgi?referer=&httpsredir=1&article=1156&context=clpe.

[32] Walter, Carl. 2014. “Was Deng Xiaoping Right? An Overview of China's Equity Markets.” p. 18.

https://onlinelibrary.wiley.com/doi/abs/10.1111/jacf.12075.

[33] Hawson, Nicholas. 2017. “China’s ‘Corporatization without Privatization’ and the Late 19th Century Roots of a Stubborn Path Dependency”. p. 11.

https://repository.law.umich.edu/cgi/viewcontent.cgi?article=3021&context=articles.

[34] Brandt, Loren, and Thomas G Rawski. 2011. China’s Great Economic Transformation. Cambridge University Press. p. 355.

LLCs/Shareholding Firms

[35] Khoo, Heiko. 2018. Is China still socialist? A Marxist critique of János Kornai’s analysis of China. p. 89-90.

https://kclpure.kcl.ac.uk/ws/portalfiles/portal/136790902/2018_Khoo_Heiko_1068757_ethesis.pdf.

[36] Szamosszegi, Andrew, and Cole Kyle. 2011. An Analysis of State-Owned Enterprises and State Capitalism in China. p. 25. https://www.uscc.gov/sites/default/files/Research/10_26_11_CapitalTradeSOEStudy.pdf.

[37] Hsieh, Chang-Tai, and Zheng Song. 2015. “Grasp the Large, Let Go of the Small: The Transformation of the State Sector in China.” p. 7-8.

https://www.brookings.edu/wp-content/uploads/2016/07/2015a_hsieh.pdf.

Examples of the Shareholder/LLC system at work

[38] “CICT”, China Govt Services.

https://govt.chinadaily.com.cn/s/201812/05/WS5c07928c498eefb3fe46e304/china-information-and-communication-technologies-group-corporation-cict.html.

[39] SMIC, “Announcement of 2022 annual results”. p. 96.

https://www1.hkexnews.hk/listedco/listconews/sehk/2023/0328/2023032801249.pdf.

[40] CNN, McDonald’s is investing more in China to tap ‘tremendous opportunity’.

https://www.cnn.com/2023/11/21/business/mcdonalds-china-stake-prospects/index.html#:~:text=The%20deal%20to%20acquire%20investment,ownership%20with%20a%2052%25%20stake.

[41] Changhong Jiahua Holdings Limited, Annual Report 2020. p. 69

https://ir.changhongit.com/pub/resource/application/2021042001499.pdf.

wanderful